This article was paid for by a contributing third party.

Distributed ledger technology in regulatory reporting

Satisfying regulatory demands can be made cheaper and more straightforward via distributed ledger technology as regulatory reporting has a transformational effect on the regulatory value chain. Maciej Piechocki, Moritz Plenk and Noah Bellon of BearingPoint discuss the challenges that must be overcome for this to be achieved.

Regulatory reporting of financial transactions is one of the key tasks in post‑trade processing for financial institutions. Satisfying increasing regulatory demands is challenging and expensive for banks. The most recent implementations of new regulatory requirements further increase the complexity and effort needed to cope with banking regulation.

From a supervisory perspective, sufficient data quality is crucial to providing reliable analysis of the stability of the banking system. Regulatory norms such as AnaCredit, the revised European Market Infrastructure Regulation (Emir II) and the revised Markets in Financial Instruments Directive (Mifid II) indicate that banking supervision is heading towards more granular data, further increasing the importance of data quality. Moreover, the timely availability of reporting relevant data needs to be guaranteed to enable regulatory authorities to act in a timely manner.

The current regulatory reporting process, with a variety of regulatory reporting softwares and data models on the banks’ side, as well as the requirement for financial institutions to report transactions individually, has led to the quality of the reported data to be insufficient: it often requires further processing steps to make it useable. Beyond that, there is a time lag between execution and the reporting of a trade.

These challenges can be overcome by utilising distributed ledger technology (DLT), which has the capabilities to increase data quality and reduce manual effort because of its unique combination of characteristics. Moreover, it enables real‑time data reporting. Its main characteristics include transparency, immutability, a single source of truth and programmable smart contracts, which lead to the facilitation of regulatory reporting (see figure 1).

Using the technical possibilities and capabilities of programmable smart contracts, regulatory legislation can be programmed as a precondition for post‑trade processing. When combined with the immutability of data stored ‘on-ledger’ and the transparency of shared facts between trading counterparties, data reconciliation is minimised and the process requires less manual interference.

In a post‑trade environment for processing regulatory reporting – to which every bank of a network is connected – there would be no need to manually match transaction data or complete forms to be sent to trade repositories, which then check for possible deviations. If two banks execute a trade in this network, the trading counterparties always have identical, up‑to‑date relevant data on their ledgers simultaneously.

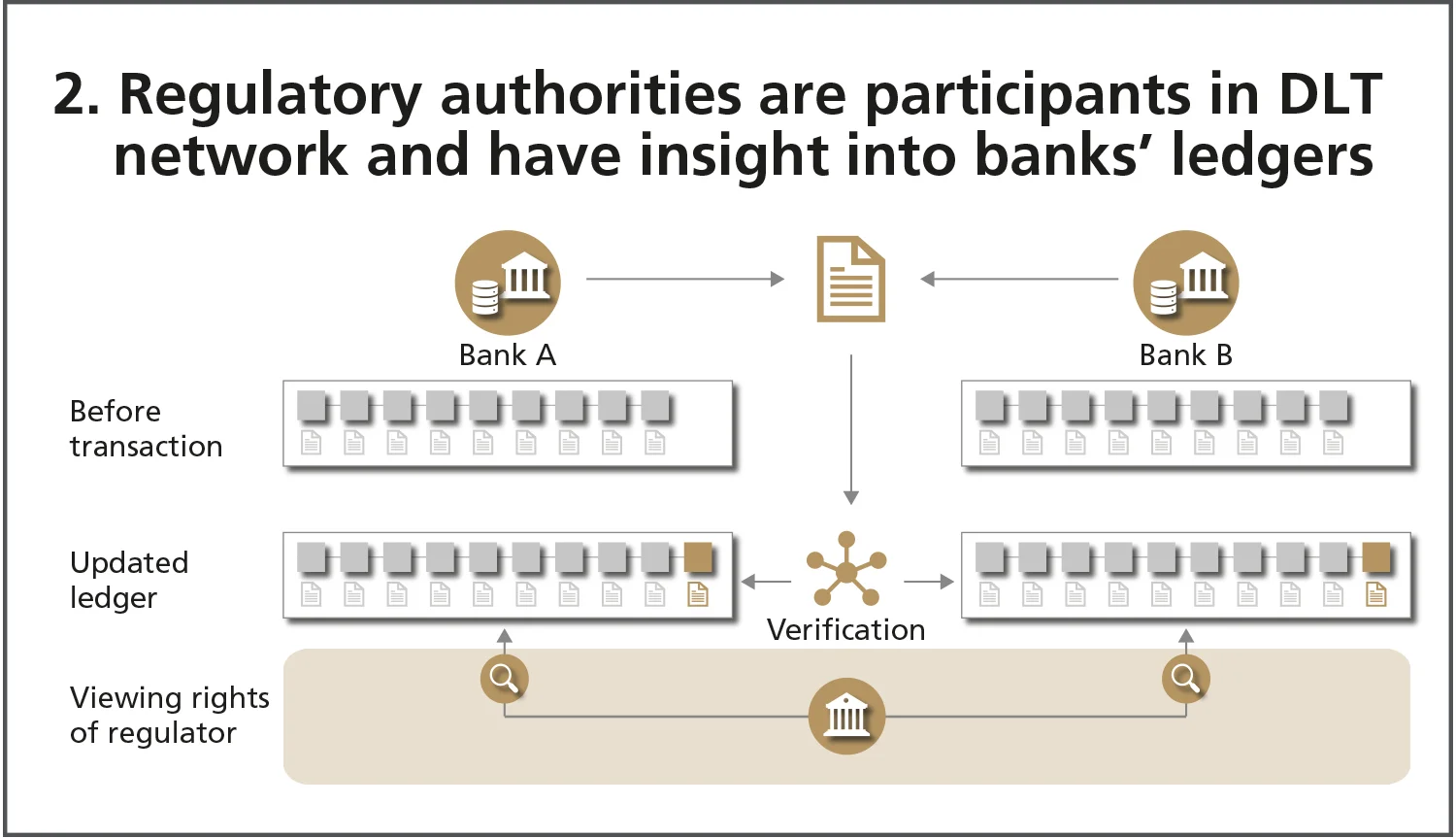

Hence, double reporting can no longer take place. Once the parties agree on a transaction report, it is submitted to the network and both ledgers are updated with the same data. Consequently, the DLT environment generates a single point of truth and guarantees no trading counterparty can have different information about transactions. The regulator is then provided with consistent and correct data at the most granular level. As a result, the overall data quality in regulatory reporting increases. Moreover, the utilisation of DLT could replace form‑based reporting as the need to actively send reports to the supervisors becomes obsolete. If the regulator is a participant of the network as a node with special viewing rights into the ledgers of banks, it has direct access to reporting relevant data. This approach removes the necessity for banks to send regulatory reporting forms to authorities because the regulator has direct access to validated transaction data of banks. Therefore, regulating entities have real‑time access to relevant data (see figure 2). From an analytical perspective, this means the regulator and financial institutions have data available on the most granular basis, making data analysis more reliable.

In addition, the smart contract rules prevent the submission of data that does not meet regulatory requirements or a mismatch of reporting data. Because of the properties of smart contracts, it is not possible to provide inconsistent data, preventing all errors in advance. On one hand, this leads to a tremendous decrease in reporting effort, because the data collection and aggregation, and subsequent examination and correction of reporting data can be eliminated. On the other, it prevents the reporting of false data to the regulator, further decreasing data quality issues from a supervisory perspective.

These capabilities promote a more efficient, less time‑consuming regulatory reporting process with enhanced data quality.

Not only is building up a DLT‑based network for regulatory reporting interesting for financial institutions and regulators of one legal sphere, but it could also increase the cross‑border efficiency of interaction and standardisation of banking regulation. The technology provides benefits for all industry participants regarding effort and quality, both for financial institutions and regulators.

Of course, for adoption of DLT in regulatory reporting to be possible, there are challenges to overcome. These should be highlighted before adopting a DLT-based regulatory reporting environment.

First, an implementation of regulatory requirements has to be functionally and technically feasible. This precondition has been tested in a proof of concept by BearingPoint Software Solutions. It has been shown that derivatives reporting, fulfilling the requirements of Emir II, is feasible with Corda – a DLT developed by the blockchain consortium R3. It also proves the feasibility of the expected real‑time availability of data for the regulator and trading counterparties. Moreover, as previously described, errors and mismatches are prevented in advance by the smart contract rules. Thus, the utilisation of DLT in regulatory reporting can create value.

A key finding of the proof of concept is that a precondition for successful implementation of regulatory law into smart contract logic is a unified data model. This is both a challenge and an opportunity. The issue arising with this condition is that all network participants must agree to the same data model with no deviations. This might lead to a high initial co-ordination effort. Once this difficulty is mastered, a unified data model reduces overall complexity of regulatory reporting, which could increase efficiency of post‑trade processing and reduce the possible scope of data discrepancies.

The second point to be taken into account is data security issues. This is especially important because the novelty of the technology increases scepticism. Even though the processed information is encrypted, the decentralised organisation of nodes in the network reduces the risk of a single central weak point. The possibility of using DLT environments that only allow permitted participants to be part of the network provides data security, but there still are some security concerns. The issues differ depending on the type of blockchain, and every design brings its own difficulties. Independently from the chosen solution, these uncertainties require investigation and testing on a large scale to dispel scepticism.

Third, a challenging issue partially related to the overall security of the system is governance. It must be clarified who defines the principles of governance and who ensures their adherence. On one hand, this would be a chance for supervisors to lead the DLT system, setting rules for participation and punishment for misbehaviour. The deployment of the regulator as the governing body of the system could also solve the risk of discrepancies about the governing entity of the system because the regulator is the most neutral body within this permissioned network. On the other hand, it shifts effort towards regulating entities, which might not be desirable from the supervisor’s point of view.

Fourth, to enable the banking industry to explore the potential and benefits of DLT, regulators need to create a technology‑friendly environment. The concept of regulatory sandboxes to test new approaches and technologies has been set up by many countries and is a promising concept to fulfilling this condition.

Solving these challenges is demanding, but not impossible. With the knowledge that implementation is feasible and regulatory reporting with DLT can solve existing problems of regulatory reporting, one precondition to enable adoption of a DLT‑based system is satisfied.

BearingPoint is confident the remaining challenges can be overcome, and believes wide adoption of DLT in regulatory reporting can transform the regulatory value chain for the better.

Read the full Central Banking FinTech RegTech Global Awards 2018 Winners In Focus report

Sponsored content

Copyright Infopro Digital Limited. All rights reserved.

As outlined in our terms and conditions, https://www.infopro-digital.com/terms-and-conditions/subscriptions/ (point 2.4), printing is limited to a single copy.

If you would like to purchase additional rights please email info@centralbanking.com

Copyright Infopro Digital Limited. All rights reserved.

You may share this content using our article tools. As outlined in our terms and conditions, https://www.infopro-digital.com/terms-and-conditions/subscriptions/ (clause 2.4), an Authorised User may only make one copy of the materials for their own personal use. You must also comply with the restrictions in clause 2.5.

If you would like to purchase additional rights please email info@centralbanking.com